Fiscal Multipliers in a Suppressed Monetary Environment: A Semi-Structural. Approach to Iraq’s Oil Economy

Iraq's economy suffers from a suppressed monetary environment that neutralizes government spending, costing 602 trillion IQD in lost GDP in 2023, making banking reform essential for growth

Executive Summary

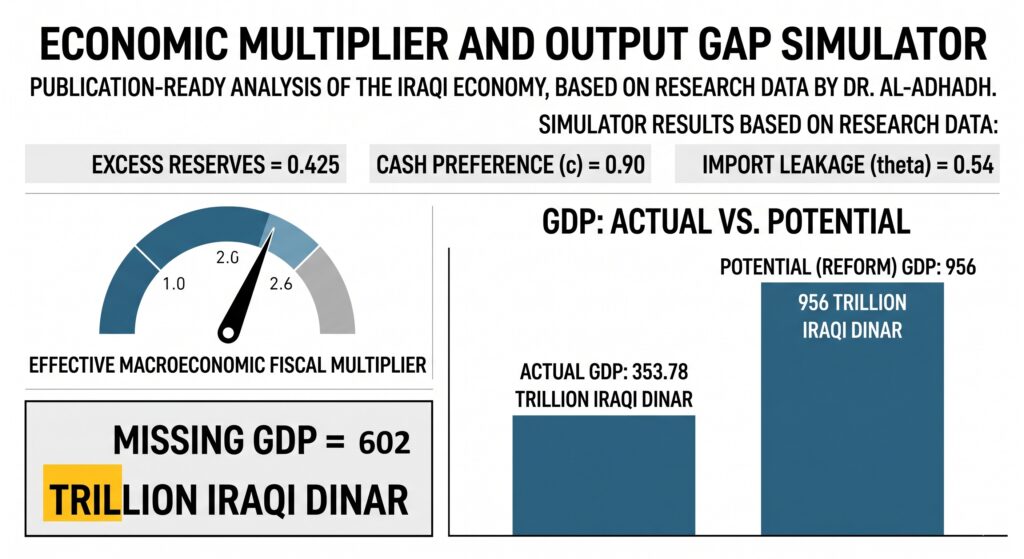

Iraq’s macroeconomic performance is fundamentally defined by its oil-dependent structure, where oil revenues drive fiscal capacity, liquidity, and aggregate demand. However, a central puzzle exists: why do massive fiscal injections fail to generate commensurate economic expansion?. This case study identifies a “Suppressed” transmission environment where a robust nominal fiscal multiplier of approximately 2.6 is neutralized by a dysfunctional monetary framework. The analysis reveals that the effective money multiplier operates at only ~23% of its theoretical capacity. Consequently, the cost of non-reform is staggering; for the year 2023 alone, the “missing” nominal GDP due to these transmission failures is estimated at 602 trillion IQD.

Table Of Content

- Executive Summary

- 1. Introduction: The Oil-Fiscal Transmission Mechanism

- 2. Theoretical Framework and Multiplier Calibration

- 3. Empirical Evidence: The Effective Multiplier

- 4. The Transmission Failure: A “Suppressed” Monetary Environment

- The Money Multiplier Constraint

- 5. Counterfactual Analysis: The 602 Trillion IQD Output Gap

- 6. The Opportunity for Growth through Reform

- 7. Conclusion and Policy Recommendations

1. Introduction: The Oil-Fiscal Transmission Mechanism

In rentier states like Iraq, oil revenues are the primary engine of the economy, financing the bulk of government spending, which in turn fuels private consumption and investment. Traditional macroeconomic models often struggle with Iraq’s volatile, data-constrained environment. This study utilizes a semi-structural approach to isolate the dominant channels linking oil revenues to GDP through government spending, liquidity amplification, and import leakages.

2. Theoretical Framework and Multiplier Calibration

The study constructs a compact model based on the national income identity ($Y=C+I+G+X-M$) tailored to Iraq’s institutional reality.

- Fiscal Identity: Government spending (G) is almost entirely financed by oil revenues (R).

- Import Leakage ($\theta$): A significant portion of demand is met through imports. Based on historical data, the import-leakage share of oil revenue is calibrated at $\theta \approx 0.54$.

By embedding these parameters, the model derives a structural “Oil-Fiscal Multiplier” of approximately 2.58. This suggests that for every unit of oil revenue injected via government spending, nominal GDP should theoretically expand by 2.58 units.

3. Empirical Evidence: The Effective Multiplier

The study validates this theoretical derivation through an econometric estimation using annual data from 2008 to 2023.

- Regression Results: Regressing nominal GDP changes on government expenditure changes yields a short-run nominal fiscal multiplier in the range of 2.0 to 2.6.

- Elasticity: A 1% increase in nominal government spending growth is associated with approximately a 0.88% increase in nominal GDP growth.

These findings confirm that Iraq’s fiscal policy is indeed active and generates a sizeable contemporaneous effect on income. However, this “effective” multiplier is significantly lower than what a functioning financial system would allow.

4. The Transmission Failure: A “Suppressed” Monetary Environment

The effective macro multiplier (2.6) is not a pure fiscal parameter; it is a joint product of a structural fiscal impulse and a monetary-financial transmission factor.

The Money Multiplier Constraint

In a fractional-reserve system with an 18.5% reserve requirement, Iraq’s theoretical upper bound for the money multiplier ($M2/MB$) is approximately 5.4. However, empirical evidence shows a starkly different reality:

- Realized Multiplier: Between 2008 and 2023, Iraq’s actual money multiplier remained consistently low, averaging close to 2.0, and falling as low as 1.10 in 2023.

- Factors of Suppression: This suppression is driven by high cash preference (currency outside banks), deep import leakages, and shallow financial intermediation.

Essentially, the banking system fails to transform base liquidity created by government spending into broad money or productive credit. Iraq is currently operating at only roughly 20% to 23% of its theoretical money-creation potential.

5. Counterfactual Analysis: The 602 Trillion IQD Output Gap

To quantify the macroeconomic opportunity cost of these rigidities, the study conducts a policy counterfactual for the year 2023.

- The Baseline (2023): Actual Nominal GDP was 353.78 trillion IQD with an actual money multiplier of 1.25.

- The Reform Target: If the money multiplier converged toward a realistic medium-term target of 3.4 (assuming modest improvements in financial inclusion and reduced cash preference), the potential GDP would scale proportionally.

- The Potential GDP: Under this scenario, 2023 Nominal GDP is estimated at approximately 956 trillion IQD.

The Gap: The difference represents a “Missing Nominal GDP” of 602 trillion IQD. This gap serves as a stark metric of the cumulative loss resulting from weak financial intermediation and the rigidities of the exchange-rate regime.

6. The Opportunity for Growth through Reform

The study further identifies that while the current effective multiplier is 2.6, the implied full-transmission fiscal multiplier ($\beta_{fiscal}$) is approximately 7.8. This means that for a given fiscal impulse ($\Delta G$), the marginal gain from reform—achieved by deepening financial intermediation and moving away from a cash-dominated economy—would be nearly triple the current output.

7. Conclusion and Policy Recommendations

Macroeconomic effectiveness in Iraq is not merely a question of the volume of state spending, but of the structural capacity of the financial system to amplify that spending.

- Prioritize Financial Intermediation: Future reforms must focus on strengthening the credit channel and reducing the overwhelming preference for physical cash.

- Address Transmission Bottlenecks: Without improving the monetary transmission channel, fiscal policy remains mathematically constrained from achieving its full developmental potential.

- Strategic Diversification: Reducing import leakage is essential to ensure that the demand impulse generated by government spending is absorbed domestically rather than flowing abroad.

In summary, the “suppressed” nature of the Iraqi economy indicates that while the fiscal engine is strong, it is currently firing in a vacuum of financial intermediation. Bridging the 602 trillion IQD gap requires a fundamental shift in how base liquidity is transformed into broad economic wealth.

Dr. Amer Aladhadh

An Iraqi-American economist, he worked as an advisor at the Qatari Ministry of Business and Trade and participated in the working group of the "United Nations Economic Commission for Europe on Public-Private Partnerships." He conducted quantitative analysis for renowned hedge funds on Wall Street. In Qatar, he also served as a business development expert, supervised the Public-Private Partnership (PPP) program, and was a member of the Qatar National Food Security Programme. Currently, he is an advisor to the Iraqi Prime Minister Mohammed Shia' Al Sudani and serves as the CEO of the Government Reform Management Cell in Iraq.

No Comment! Be the first one.